Tracking your provident fund growth manually gets confusing fast, especially when interest rates change every quarter. A GPF calculator solves this by doing the math for you instantly, showing exactly how your monthly contributions turn into a retirement corpus over time. Government employees often rely on rough estimates from old statements, but that approach rarely matches the actual numbers.

Once you understand how the calculator works, planning your contributions becomes far easier. You can see how small changes in your monthly deposit affect your closing balance years down the line. This clarity helps you make better decisions rather than waiting until retirement to find out where you actually stand.

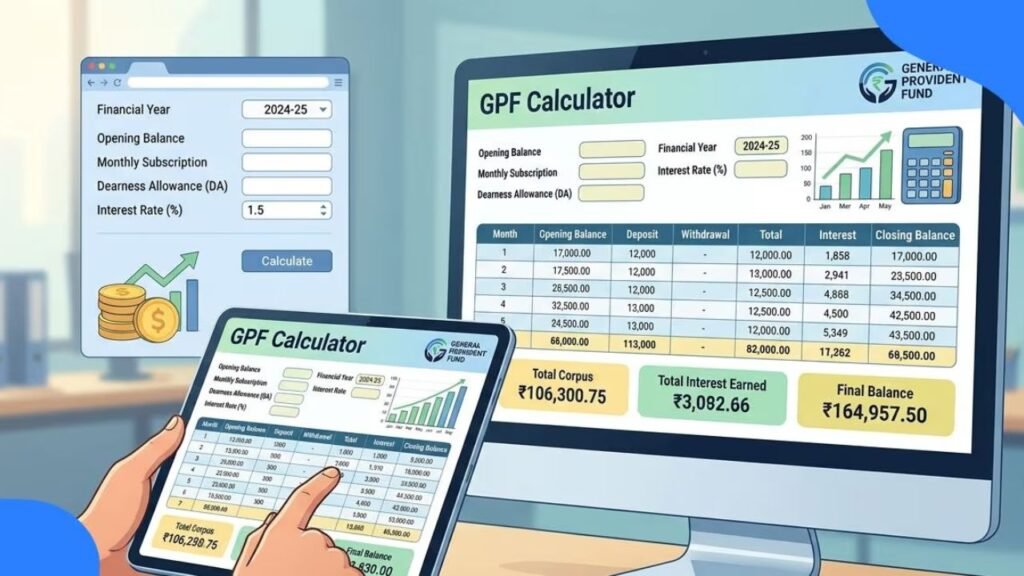

GPF Calculator: A Simple Way to Track Your Provident Fund Growth

A GPF calculator takes your opening balance, monthly contribution, and interest rate, then projects your account balance for the many years you choose. Instead of calculating interest by hand every month, the tool applies the current rate automatically and shows you a clear breakdown. This matters because GPF interest doesn’t work like a fixed deposit. It follows a monthly running balance system, so the timing of your deposits actually changes your final numbers. A calculator accounts for all of this without requiring you to understand the underlying formula yourself.

How does the GPF Calculator work?

Before you start calculating, gather a few numbers from your latest GPF passbook or salary slip. Having these ready makes the process quick and accurate.

Opening Balance and Contribution Details

- Opening balance: the amount already present in your account at the start of the financial year

- Monthly subscription, which must range between 6% and 100% of your basic pay plus dearness allowance

- Duration in years, based on how far ahead you want to project

Rate and Withdrawal Details

- Current GPF interest rate, set at 7.1% per annum for this financial year

- Advance withdrawal amount, if you plan to take one during the period

- Any change in the monthly contribution partway through the year, if applicable

Once you enter these details, the calculator shows your total balance, total withdrawals, and closing balance for the period you selected.

Sample GPF Calculation With Numbers

Numbers make more sense when you see them applied to a real scenario. Here’s an example using a modest monthly contribution alongside a partial withdrawal within the same year.

| Opening Balance | Monthly Subscription | GPF Rate | Years | Advance Withdrawal | Total Balance | Total Withdraw | Closing Balance |

| ₹1,00,000 | ₹12 | 7.1% | 1 | ₹25,000 | ₹1,07,254 | ₹25,000 | ₹82,254 |

Notice how the interest still adds to the balance despite the small contribution amount. However, the withdrawal directly cuts into the closing figure, which shows why timing withdrawals carefully matters just as much as increasing your monthly deposit.

GPF Information and GPF Balance Check on Mobile

Checking your GPF balance on mobile no longer requires waiting for paper statements from your accounts department. Most state governments and central departments now offer online portals where you can view your ledger anytime.

Steps to Access Your GPF Account Online

- Open your state’s Accountant General office website or your department’s e-service portal

- Log in using your GPF account number along with your registered credentials

- Locate the GPF ledger or passbook section within your dashboard

- Review your current balance, contribution history, and interest credited for each year

Some departments send SMS alerts whenever a contribution or interest amount gets credited. So even without logging in constantly, you stay updated on your account activity.

About the General Provident Fund Scheme

The General Provident Fund exists as a mandatory savings scheme for employees working in central government, state government, and certain union territory administrations. It started back in 1956 and continues to operate under the Ministry of Finance.

Each month, a fixed percentage of your basic salary and dearness allowance gets deducted and added to your individual GPF account. This amount then earns interest until you retire, resign, or, in unfortunate situations, until your nominee receives the balance. Unlike EPF, which covers private-sector employees, or PPF, which any citizen can open, GPF remains exclusive to government employees.

GPF Interest Rate for the Current Financial Year

The GPF interest rate currently sits at 7.1% per annum for this financial year, and it has stayed consistent since the first quarter. The Department of Economic Affairs reviews this rate every quarter and releases an updated notification whenever a change occurs.

This rate doesn’t apply only to GPF. It also covers the Contributory Provident Fund, All India Services Provident Fund, State Railway Provident Fund, and the General Provident Fund for Defence Services. So regardless of which of these funds you contribute to, the same rate applies across the board.

GPF Interest Rate Trend Over the Years

Looking at how this rate shifted over the past decades gives useful context for anyone planning long-term savings through GPF.

| Period | Interest Rate |

| 1986–2000 | 12% |

| 2019-20 | 7.9% |

| 2022-23 | 7.1% |

| Q1 (Apr–Jun 2025) | 7.1% |

| Q2 (Jul–Sep 2025) | 7.1% |

| Current Rate | 7.1% |

The rate peaked at 12% between 1986 and 2000 due to higher inflation levels during that era. Since then, it has gradually declined, closely following the movement in government securities yields rather than staying static.

Monthly Interest Calculation Rules for GPF

GPF interest doesn’t apply directly to your yearly closing balance. Instead, it works every month, calculated on the balance held between the 5th day and the last day of each month. The government then credits this accumulated interest once a year, typically on March 31.

This detail trips up many subscribers. If your deposit reaches the account after the 5th of the month, that particular contribution might miss out on interest for that month entirely. Over several years, this small gap can quietly shrink your total corpus more than most people expect.

Real-Life Example of Contribution Timing

Picture two employees contributing identical amounts every month. One deposits before the 5th consistently, while the other faces payroll delays and deposits around the 10th. Over two decades, the first employee earns a few extra months of interest annually compared to the second. This difference seems small each year, yet it adds up meaningfully by the time both employees retire.

Common Mistakes Employees Make With GPF

Many subscribers lose potential savings simply by overlooking small procedural details. Recognizing these mistakes early helps you avoid repeating them for years.

- Ignoring the 5th-day interest cutoff, which delays when late deposits start earning interest

- Skipping regular passbook checks, allowing deduction errors to go unnoticed

- Withdrawing large amounts without calculating the long-term effect on future interest

- Mixing up GPF withdrawal rules with NPS or EPF rules, since each scheme works differently

- Forgetting to update nominee details after marriage or other major life changes

Avoiding these issues doesn’t demand extra effort. It simply requires checking your account periodically and running a calculation before making withdrawal decisions.

Best Practices for Managing Your GPF Account

Building a few consistent habits makes a noticeable difference in how much your GPF account grows by retirement.

- Deposit your monthly contribution before the 5th whenever your payroll schedule allows it

- Review your online statement or passbook at least twice each year

- Run your numbers through a calculator before applying for any advance withdrawal

- Match your contribution percentage with your actual retirement goals instead of the bare minimum

- Update nominee information promptly whenever your personal circumstances change

None of these steps takes much time, yet together they protect your savings from small, avoidable losses.

GPF vs EPF vs PPF: Quick Comparison

Since people frequently confuse these three schemes, a direct comparison clears up the differences quickly.

| Feature | GPF | EPF | PPF |

| Eligibility | Government employees only | Private-sector employees | Any Indian citizen |

| Current Interest Rate | 7.1% | Set separately by EPFO | Set separately by the government |

| Managing Authority | Ministry of Finance | EPFO | Ministry of Finance |

| Contribution Range | 6% to 100% of basic pay + DA | Fixed salary percentage | Flexible, within yearly limits |

| Tax Treatment | Section 80C, tax-free maturity | Section 80C, tax-free maturity | Section 80C, tax-free maturity |

This comparison shows why GPF fits government employees specifically, while EPF and PPF serve entirely different groups with their own contribution and withdrawal rules.

Conclusion

A GPF calculator turns confusing monthly deductions and quarterly interest changes into something you can actually understand and plan around. Once you know how your contributions, withdrawals, and interest rate interact, managing your retirement savings stops feeling like guesswork. Pair regular use of a GPF calculator with quick mobile balance checks every few months, and you’ll always know exactly where your retirement corpus stands, without waiting for annual statements or depending on someone else to explain the numbers to you.

Also Read About: Develop OXZEP7 Software: Building Secure, Scalable, and Future-Ready Applications